Military Finances 101: Another New Tax Form!

Taxes Managing Your FinancesAs you may be aware, the One Big Beautiful Bill Act (OBBBA...but I'll call it HR-1) added some new deductions. They are deductions from tip income, overtime, car loans and an enhanced deduction for seniors. While admittedly, these deductions won't apply to many Active Duty Military Members (at least I never got tips or overtime when I was in) except maybe the interest you're paying on your brand new smokin car. But some could apply to your family members. I'm not going to go into too many of the specifics of the deductions as I'll cover them in another blog post.

But there are two things you need to know.

- You'll need to figure out your over-time and tips. They won't be reported on your W-2

- You'll have to complete a new form; Schedule 1-A

Figuring Out Tips and Overtime

You employer is not required to and probably won't report your overtime on your W-2. You'll be responsible for going through your old pay stubs and figuring out how much overtime you were paid. You still have all your pay stubs, right?

You might be able to figure out your tips from your W-2, if you report tips to your employer. The W-2 does have a box (Box 7) that shows your Social Security tips. If you report all your tips to your employer, then you're covered. If any or all of your cash tips aren't reported to your employer, you'll need to track them for the deduction (and report them as income too).

Bottom line: The math is on you (or your child if appropriate)

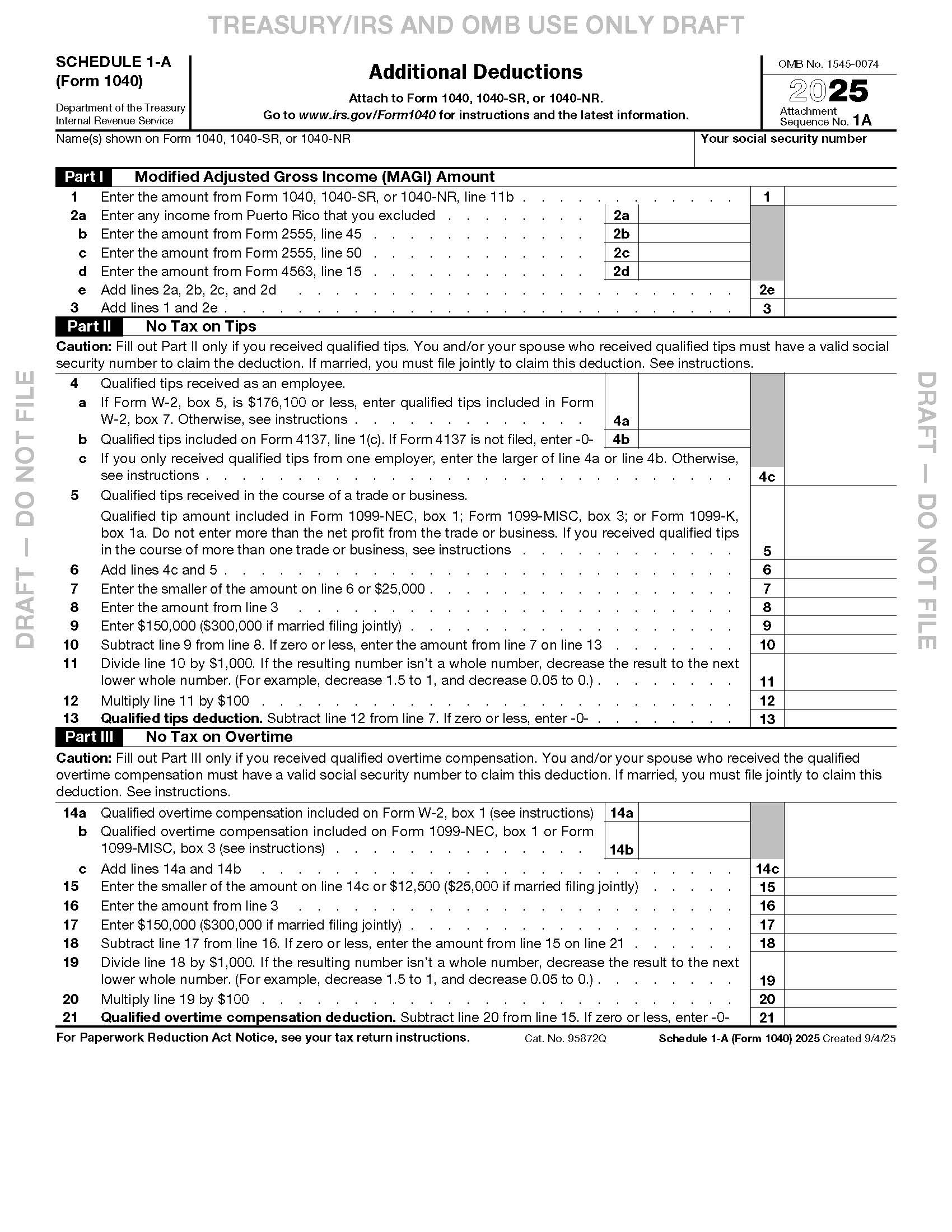

Completing Schedule 1-A

As mentioned, there is a new form, Schedule 1-A and we think it will look something like this:

There is also a page 2, but I won't post that.

I realize that most of you will use a tax preparer or tax software to complete Schedule 1-A. But it is always a good idea to at least have a fundamental idea of what is going on, on the form.

Initially, you (or your computer) will calculate your Modified Adjusted Gross Income (MAGI). For most of us, that will be the same as Adjusted Gross Income (AGI). Then the Form addresses all the new deductions.

Part II addresses No Tax on Tips. As mentioned above you'll need to calculate the tips you received. Then you'll compare the amount of tips you can exclude ($25,000) to your actual tips and whether your income is too high to claim the deduction.

Part III addresses No Tax on Overtime. It is pretty similar to Part II. Max deduction and any limits to the deduction due to your MAGI.

Part IV addresses No Tax on Car Loan Interest. On this one you'll need to verify your car (not you) qualifies for the deduction. To do this, you'll need the VIN. Then you'll calculate the allowed deduction, which is limited and any limitations based on income...which are lower than the limitations above

Finally, Part V covers the Enhanced Deduction for Seniors. Qualifying for this one is based on your age (which should be pretty simple to figure out). There is a limit based on MAGI (which is the lowest of all the deductions above).

Once you complete all the applicable sections on Schedule 1-A, you'll enter the total amount on your Form 1040 between your AGI and your itemized or standard deduction (I'm pretty sure)

Wrapping it Up

It's just another tax form to complete and Congress' and the IRS' attempts to make your life just a little simpler.

Military Finances are Different

The new deductions apply to all taxpayers. That isn't always the case. Active and Retired Military Members have unique tax and other financial benefits. That is why we think Active and Retired Senior Military Officers and NCOs should work with a financial planning firm that deals with your unique issues each and every day. If you'd like to find out how we work with clients just like you, use the button below to schedule a free, initial consultation.

If you found this article useful, you might like the following blog posts:

Retired Military Finances 201: Charitable Giving Tax Treatment is Changing

Retired Military Finances 201: Doing the 529 TwoStep

Retired Military Finances 401: IRA Considerations in the Year Dad (or Mom) Passes Away